.svg)

What are consumers saying about interactive teller machines?

In a recent study, Forrester research surveyed 1,213 US bank/credit union customers with personal checking and/or savings accounts with financial institutions that offered transactions with video bankers at interactive teller machines. The goal was to determine their thoughts, sentiments and behaviors about interactive teller machines. The survey group was 57% female/43% male residing in regions across the continental US and Alaska.

Here are some of the survey’s findings:

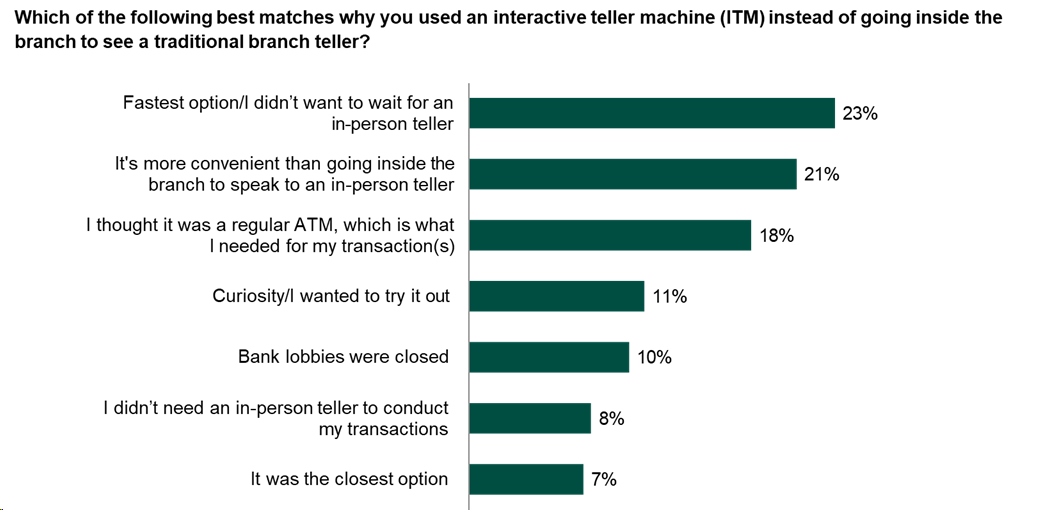

• 23% of respondents cited speed and 21% cited convenience as their top motivators for using an ITM rather than going into the branch for in-person assistance.

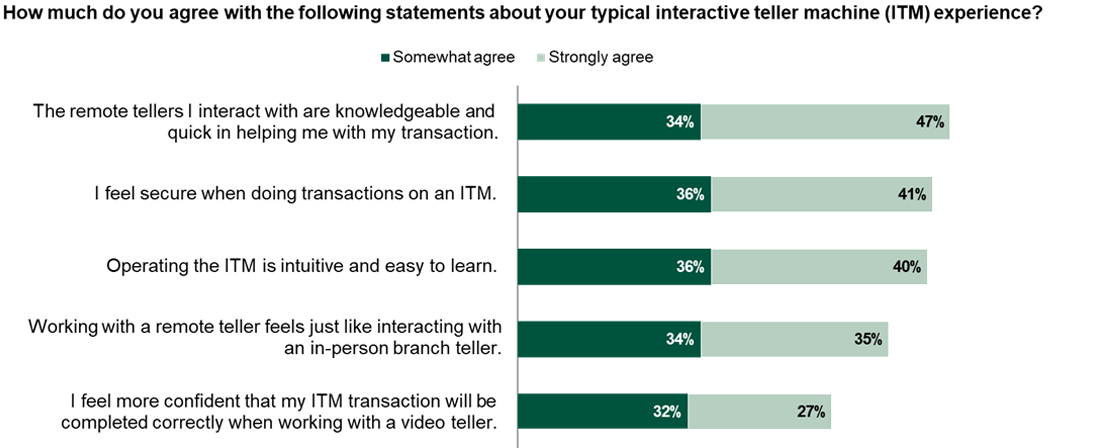

• 69% agree or strongly agree that “working with a remote teller feels just like interacting with an in-person branch teller.”

• 81% of those who have interacted with remote tellers at ITMs agree or strongly agree that they are “knowledgeable and quick in helping me with my transaction.”

• 75% of those who have used an ITM for both basic and advanced transactions said their experience of it was as positive or better than with an in-person teller. 36% said the ITM experience was better.

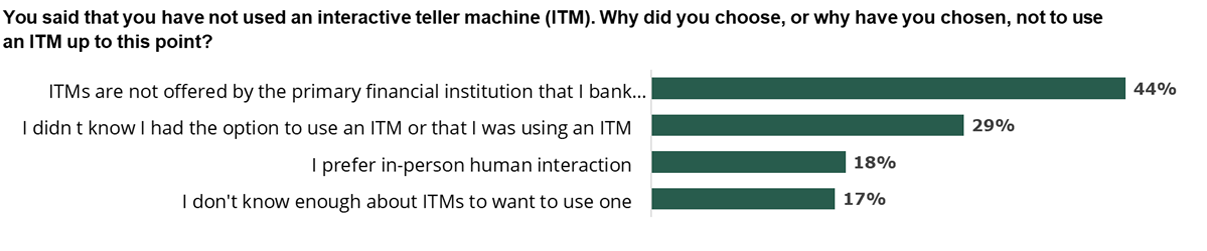

• 44% of respondents who don’t use ITMs said they don’t because their primary bank or credit union doesn’t offer them or because they didn’t know they had the option.

Other survey findings

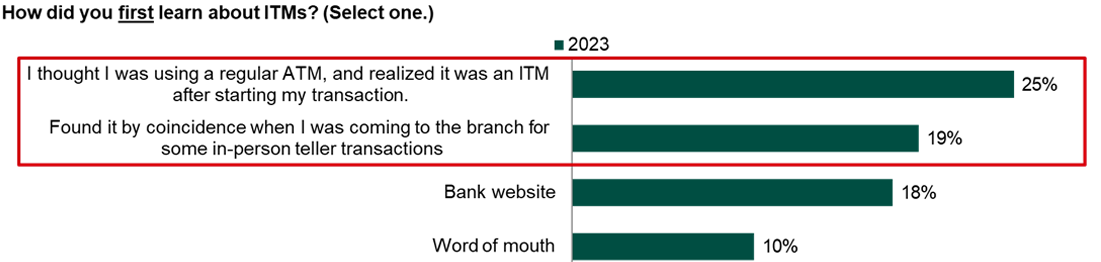

Nearly half of first-time ITM exposures were “coincidental”, meaning they didn’t specifically look for an ITM but used it on the spur of the moment.

Most respondents said they intend to continue using ITMs, but not necessarily for every transaction. Frequent ITM users said they prefer them to in-person tellers. Most said they don’t use them often (likely because many of the transactions they make are simple), but they like having the option for the types of transactions they would typically make in person.

Related: The new interactive teller machines: where convenience meets the human element

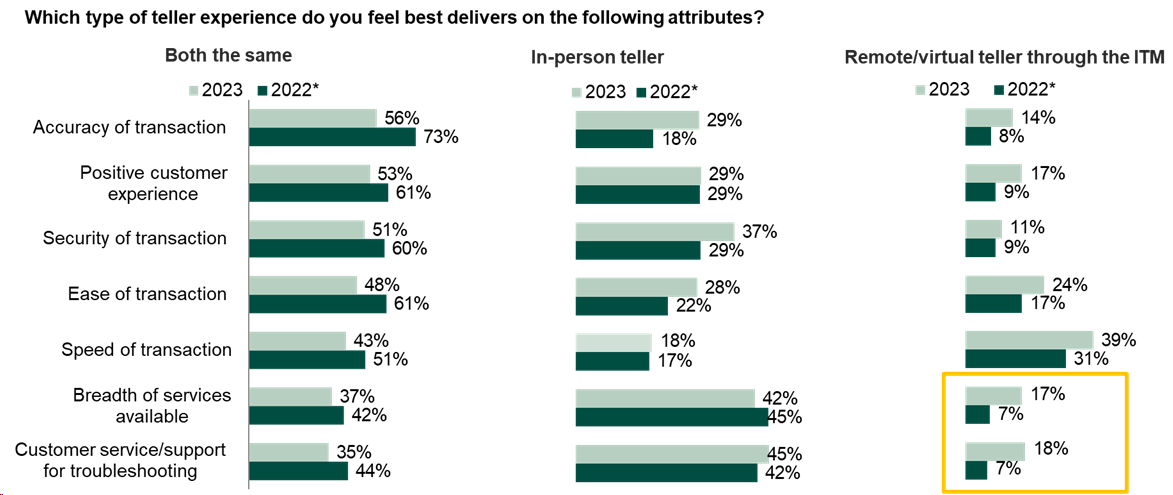

Respondents gave both ITM tellers and in-person tellers high marks for accuracy, ease of use and security.

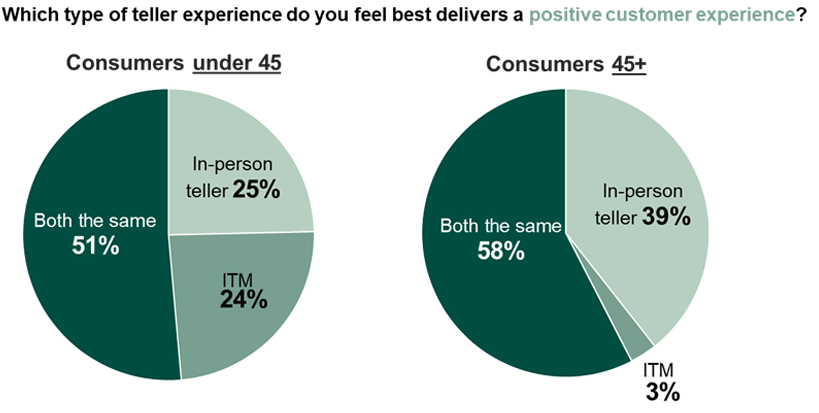

Younger respondents ranked ITMs higher for positive customer experiences, older respondents ranked in-person interactions higher.

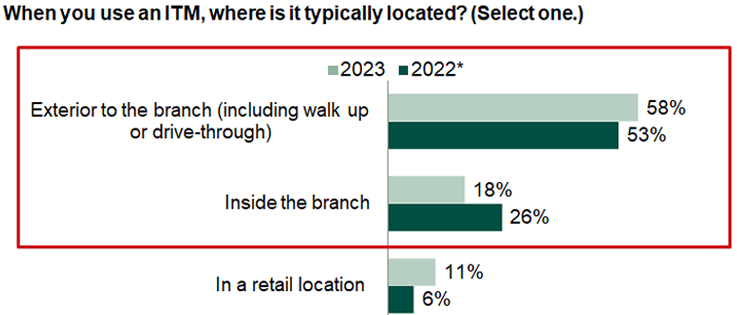

Several respondents said they tend to use ITMs at exterior or standalone placements rather than inside physical branches—once they’re inside branches, they tend to gravitate toward in-person tellers. But these percentages shifted a bit between 2022 and 2023, which may be an indicator that familiarity and usage experience are making people more comfortable walking by the teller line to get to the ITM.

Interpreting the data: what can we learn from the survey results?

Two key conclusions can be drawn from the data.

First, that customers clearly prize convenience over all other benefits and see ITMs as providing a high level of convenience. All the attributes study participants said were important to them were about convenience: faster service, easy access to staff with sales and advisory skills, more in-person service hours and access from underserved locations.

Customers say they care most about faster service, easy access to staff with sales and advisory skills, more in-person service hours and access from underserved locations.

Second, the study shows that consumers are comfortable with aspects of ITMs that we weren’t sure they would be. When ITMs were first introduced, we expected that there’d be a learning curve for customers, that they would have questions—but this was not the case. As financial institutions across the US increase the numbers of ITMs in their estates, most consumers—and most bank and credit union customers—don’t feel the need to learn what an ITM is or be reassured about what it does. They just step up to their FI’s banking kiosk and read a message that says, ‘press to talk with a banker or insert your card to use the ATM’ and do so.

The survey didn’t reveal any customer concern about where the person on the screen was located. Clearly, it didn’t matter to users whether the person helping them was in the drive-up booth, a branch across town or even working from home because the interaction felt personal, comfortable, normal, helpful and happened quickly, just as they wanted.

Customers aren’t saying, “We want more ITMs”, they’re saying they want more convenience. Banks and credit unions are using ITMs to deliver that convenience, and their customers like it.

Like the smartphones we didn’t know we wanted until we experienced what they could do for us, consumers didn’t know that what they wanted was an ITM. They just want fast service and increasing options, so when they go to a banking kiosk and see an ITM they use it.

The comfort level with video screens is already there, since customers who’re accustomed to using the drive-up at their branches are already comfortable talking with a teller over video while making a transaction. After all, banking drive-ups have been around for over a century and fried chicken drive-ups have been around even longer.

What banks and credit unions are saying about the Forrester survey

Overall, the survey confirmed what US financial institutions that offer ITMs had been hearing from their customers: that their customers like the speed and convenience ITMs provide and feel increasingly comfortable using them.

“It helped us understand how ITMs are used and how to effectively deploy them into our footprint. The data provided clarification that customers are okay with using ITMs for speed and accuracy. And customers are actually okay if a bank employee is virtual versus in person at their local branch.”

—VP ATM/ITM channel, of a southeastern US bank

“It helped us validate metrics that will impact our business. It also helped us separate signals from the noise in terms of how we reach out to our customers to improve our own standards of measurement.”

—SVP Retail and ATM/ITM of a midwestern US credit union

Implications for financial institutions

Customer demand for better hours and faster service is driving increased adoption of ITMs at banks and credit unions across the US. In addition to customer experience benefits, improved efficiency and support of branch modernization are other key drivers of this trend:

• 84% of financial institutions that have adopted ITMs say they have seen improved branch efficiency.

• 47% say they have improved customer convenience.

• 41% say they have improved their competitive advantage and 40% say they have supported branch modernization efforts.

We’ll explore financial institutions’ responses to the Forrester survey on a variety of ITM-related topics, including anticipated benefits, real-time benefits, challenges, learnings and business expectations going forward in the next issue of CONNECT.

Let’s explore what’s possible for your business. Our team is ready to connect and discuss tailored solutions that meet your goals.

Thank you for reaching out. A member of our team will be in touch shortly to continue the conversation.