Insights

Delivering fresh perspectives on the industry's biggest challenges.

article

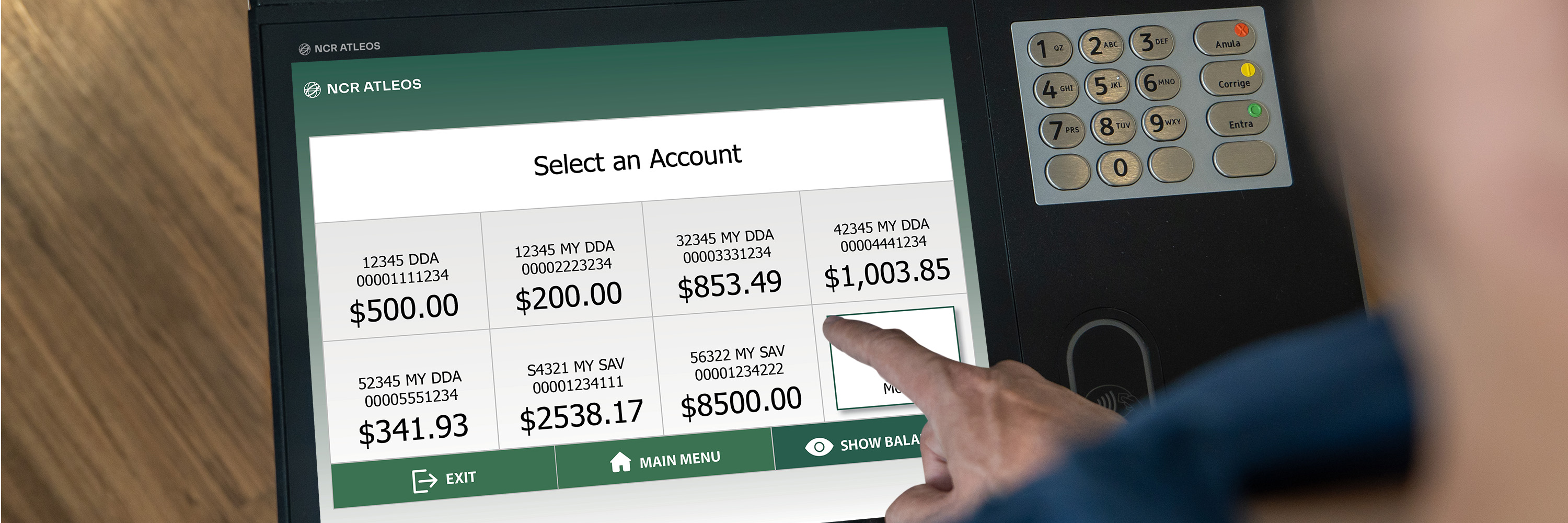

The many roles of ATMs for banks, credit unions, fintechs and communities

Learn how utility banking, innovation and AI are reshaping ATM strategy for banks, credit unions and fintechs.

.jpg)

.jpg)

.jpg)

%20(1).jpg)

.jpg)

.jpg)

.jpg)

%20(1).jpg)

Keep on top of the latest trends and developments in self-service banking to drive success

All insights

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Cash, for resiliency when digital payment systems fail

When digital payment systems fail, it’s cash to the rescue.

Cash Optimization

5 steps to transform your network security

Embedded network security involves cross-functional planning and collaboration. Learn more about the approach we recommend.

Telecom & Technology

International Day of Banks: Banking for a better world

This infographic celebrates the International Day of Banks and the role FIs play in building a sustainable financial ecosystem.

Enhanced Customer Experience

Cybersecurity challenges in future enterprise connectivity

Learn how enterprises are addressing the cybersecurity concerns brought on by integrating AI and IoT technologies at scale.

Telecom & Technology

.jpg)

ATM branding hits the screen

With ATM screen branding, you can extend your reach, unlocking new opportunities for growth, visibility and customer connection with every transaction.

Fleet Modernization

Decoding the future of enterprise architecture

This report showcases the ways leaders are leveraging hybrid edge-cloud architectures to reconcile the unique advantages of each.

Telecom & Technology

Achieving competitive advantages through ATM deployment

Escaping the ATM deployment maze by consolidating services with a single expert partner

Enjoying this content?

Sign up to stay up to date on our latest articles, case studies and other value-packed content.

Thank you!

Your submission has been received.