How ATMs are helping to narrow ‘the gender gap’

The gender gap in financial services is narrowing. This year, it narrowed faster than in other recent years.

Around the world, access to financial services, education, healthcare and political standing is becoming more available to women. For many, this means increased control over their own lives and the lives of their children. But access for women that is equal to that of men remains a distant goal.

The World Economic Forum (WEF) introduced “the gender gap” in its 2006 Global Gender Gap Report as an index for tracking progress toward gender parity worldwide. The report tracked and analyzed current economic, educational, health and political opportunities and outcomes available to women compared with those available to men on a 0–100% scale, with 100% meaning full parity between men and women.

WEF's ‘gender gap’ index tracks women’s access to economics, education, health and political standing compared with men’s.

That year, WEF reported that the gap was at 64%. This meant that, according to their analysis, women had 64% of the access men had to economics (money), education, health and political standing (rights). To put it another way, women had 36% less opportunity in these areas than men.

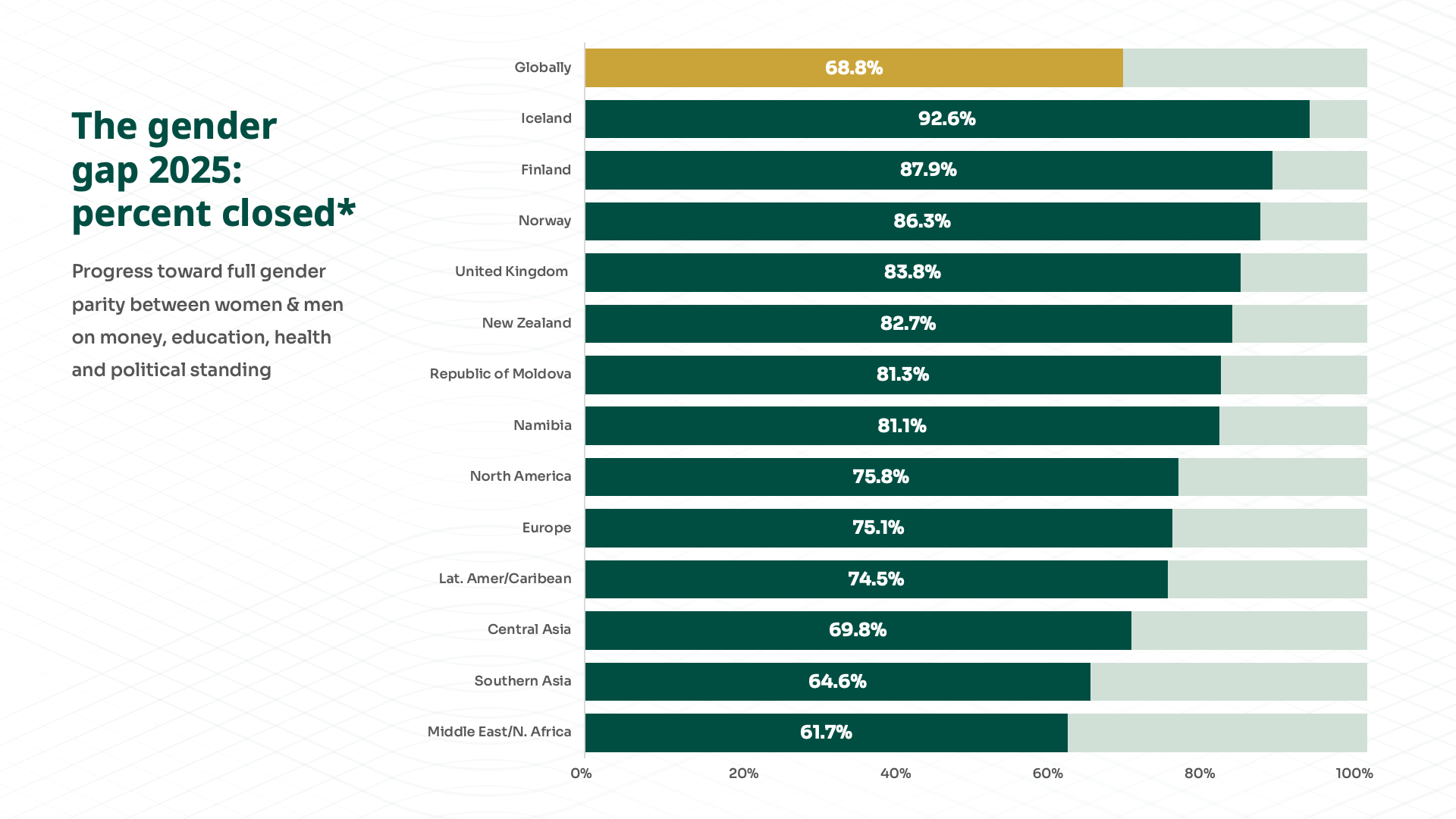

The latest edition of the report, published in 2025, showed the gender gap narrowing by 0.3%—more than in other recent years. It has now risen to 68.8% (meaning that women globally have 68.8% of the access men have in the four key areas analyzed). Yet at the current pace, full gender parity is an estimated 123 years away.

Using self-service financial access to remove barriers for women

Self-service financial access has been helping to close the gender gap through the expanding availability of ATMs. As financial institutions, government entities and non-profits work to finish closing the gender gap in economic opportunity, self-service continues to hold rich opportunities for the financial services industry—and for women around the world.

It’s one of the most effective tools for expanding financial inclusion, especially for women. ATMs and other smart kiosks offer private, secure and convenient ways to access financial services, particularly in regions where visiting a branch may be culturally restricted or geographically challenging because women still face legal, cultural and institutional barriers to these services.

ATMs offer private, secure, convenient access to financial services in regions where visiting a branch may be culturally restricted or geographically challenging.

Studies around the world have consistently shown a sizable gap in the financial health of men and women. Women are more likely to be financially vulnerable than men (24% vs 17%), meaning they struggle in nearly all areas of their financial lives.

Women are five to eight times more likely than men to have their employment affected by caregiving responsibilities for children and elders. Career breaks for caregiving often result in gaps in retirement savings and credit history, which can in turn reduce eligibility for loans and financial products needed to grow a business. In an Australian study, women who took career breaks for caregiving experienced downward mobility in salary and status, with longer breaks leading to greater income penalties, and a study in India found that women who took a five-year career break at age 25 would accumulate a pension pot 33% smaller than their male counterparts.

In developing economies, only 68% of women have financial accounts, compared with 74% of men, limiting their ability to build credit histories.

But financial inclusion is more than being able to open an account. It’s also about access to credit, insurance, savings, investment tools and the ability to build long-term financial security. ATMs often serve as the first point of contact with formal financial systems for unbanked or underbanked women, providing access to:

- Cash withdrawals and deposits

- Balance inquiries and mini-statements

- Bill payments and mobile top-ups

- Government benefit disbursements

For financial institutions and technology providers, expanding and modernizing ATM networks is a practical, scalable way to improve access and equity. In rural and underserved areas, self-service solutions can be transformative. When paired with biometric authentication or mobile integration, they reduce the need to carry formal identification documents, another common barrier for women.

And when those ATMs are ITMs, or interactive teller machines, they also offer the appeal of being able to look a real person—a remote teller—in the eye while you talk. And eye contact, even when mediated through video, can have a reassuring effect, particularly for women, in situations that might feel unfamiliar or challenging, according to recent studies.

Where the gap is closing fastest

Some regions around the world are making faster progress on closing the gender gap than others. Latin America and the Caribbean are leading the way, projected to reach gender parity in just 57 years. Europe and North America follow closely. But in Central Asia and the Middle East and North Africa, the timeline stretches beyond 180 years.

It’s interesting to note that some lower-income countries are outperforming wealthier ones on this count. Bangladesh, Ethiopia, Mexico and Saudi Arabia are among the fastest movers. This suggests that political will and targeted policy can be more decisive than income level alone.

The business case for closing the gap

But gender parity isn’t only a social imperative—it’s also a business one.

Women now outpace men in higher education globally. Yet these gains have yet to move women significantly closer to gender pay parity, earning on average 20% less than men. That’s a disconnect between capability and opportunity that can limit innovation, customer insight and growth.

Companies that prioritize gender equity tend to outperform their peers. They’re more resilient, more adaptable and better at serving diverse markets. In financial services, where trust and usability are everything, inclusive design isn’t optional—it’s essential to institutional performance in a tight-margin environment.

What’s working—and how the industry can accelerate it

From a technology standpoint, expanding self-service access points—ATMs, other kiosks and mobile-first platforms—can dramatically increase women’s financial autonomy. These tools are especially impactful when designed with accessibility, privacy and local context in mind.

The World Economic Forum and other global organizations are working with governments and businesses through ‘gender parity accelerators’—programs designed to fast-track women’s participation in the workforce and leadership. These initiatives focus on pay equity, career advancement and inclusive hiring practices.

Video-enabled kiosks can have a reassuring effect in situations that might feel unfamiliar or challenging.

There’s also a growing push to support nonlinear career paths. That means recognizing and supporting re-entry into the workforce after caregiving breaks and investing in care infrastructure so women don’t have to choose between family and financial independence.

Countries leading the way in gender parity

Here are some compelling examples from The Global Gender Gap Report 2025 that illustrate how financial inclusion and gender parity are evolving around the world.

Iceland has been the global leader in closing the gender gap for the 16th consecutive year, having closed 92.6% of its gender gap. It is the only country to have surpassed the 90% threshold.

Finland and Norway follow closely, with scores of 87.9% and 86.3%, respectively, driven by strong performance in education, health and political representation.

New Zealand ranks 5th globally with 82.7% of its gap closed and is one of the few non-European countries in the top 10.

Other countries making rapid progress include:

The United Kingdom jumped from 14th to 4th place in just one year, closing 83.8% of its gap. This was largely due to a gender-equal cabinet and a significant rise in women’s parliamentary representation—from 47.4% in 2024 to 64.3% in 2025.

Republic of Moldova moved up to 7th place, closing 81.3% of its gap. It has more than tripled its political parity score since 2006.

Namibia, ranking 8th, has closed 81.1% of its gender gap, showing strong performance in both political and economic participation.

What this means for financial services leaders

For those building the future of financial services, the message is clear: inclusion fosters innovation.

Designing products that work for women—especially those in underserved communities—opens up new markets and builds long-term customer loyalty. It also means rethinking how we measure creditworthiness, how we design onboarding experiences and how we support small business owners.

Financial institutions, fintechs and technology providers all have roles to play in closing the gap. That includes investing in infrastructure, reimagining customer journeys and embedding equity into product design from the start.

The road ahead

The gender gap in financial inclusion is real but not inevitable. With the right data, the right partnerships and the right mindset, the financial services industry can help close it faster than the current 123-year projection.

The tools are already in our hands. Now it’s about how we use them.

Let’s explore what’s possible for your business. Our team is ready to connect and discuss tailored solutions that meet your goals.

Thank you for reaching out. A member of our team will be in touch shortly to continue the conversation.